Over the next few blogs, I will discuss the concept of a new approach to fraud risk assessment with a new model. This is for those who are open-minded to change. It is important to note that it is not my goal to say what we are doing is right or wrong. However, we as a profession must be willing to evolve in our thought process. If you study all the fraud literature, you will see a gradual change or improvement in the fraud risk guidance. What I am proposing should be the next leap forward for our profession.

Over the next few blogs, I will discuss the concept of a new model and a new approach to fraud risk assessment. Two things to note. First, you must be open-minded to change. Second, it is not my goal to say that what we are doing is wrong. As with so many theories, change is necessary. Fraud in companies has evolved and we must be willing to evolve along with it.

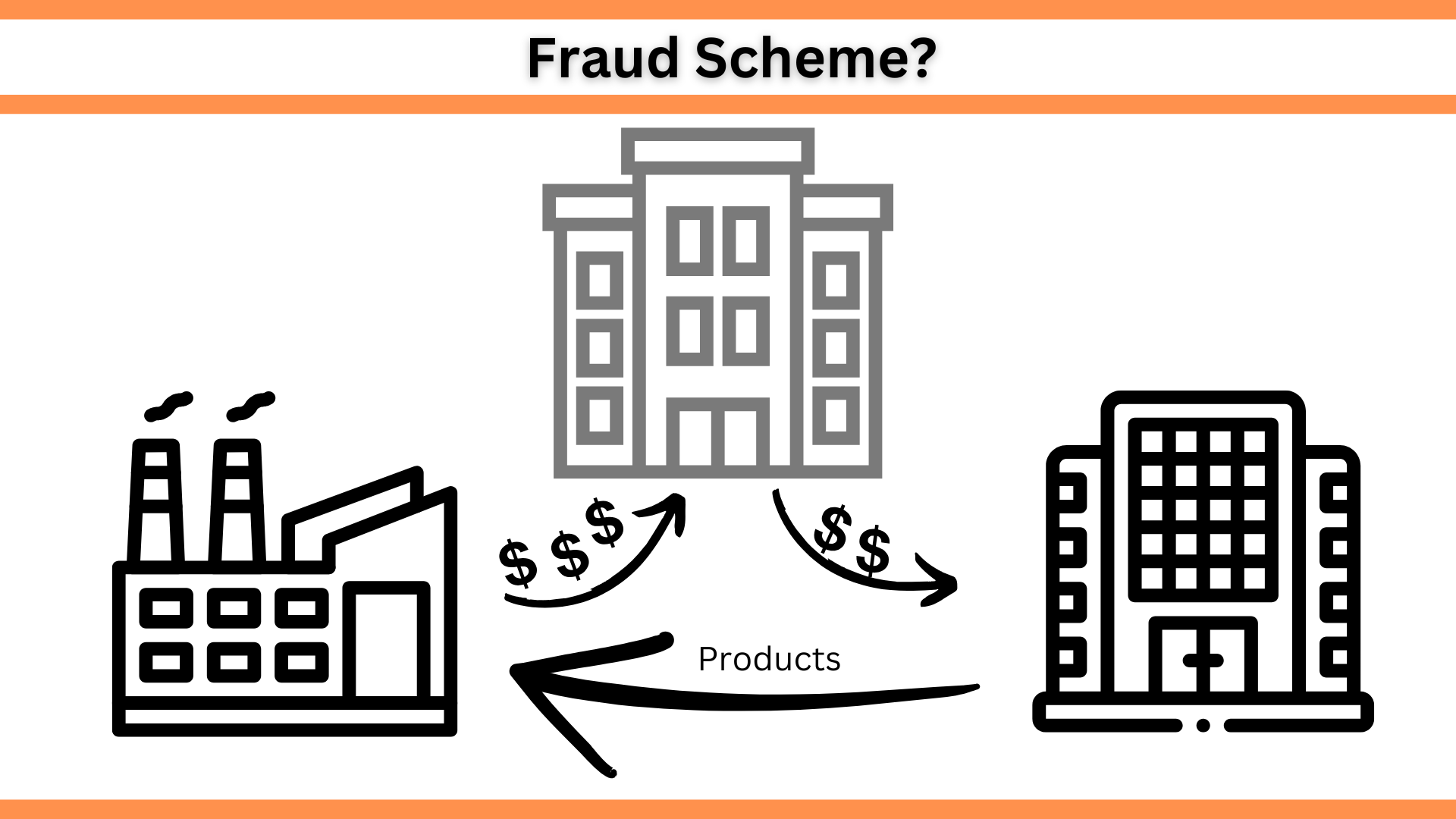

In one sense, there is nothing new when it comes to misstatement of revenue in financial statements. With a little effort, you can find real-life examples of these schemes in both publicly traded companies and privately held companies. How the scheme is perpetrated may differ by industry or by company. How the scheme is concealed may differ by industry or by company. So, how can auditors uncover these schemes?

Before I start, let me explain that in this blog I will not provide any answers to the phrase “Deeper Understanding of Fraud Schemes.” Rather, I will only raise questions regarding the phrase. To be honest, If I was a CAE, I am not sure what the profession wants me to do.

With that said, I praise the profession in recognizing the importance of gaining a deeper understanding of fraud schemes facing our companies. Maybe, I am talking out of both sides of my mouth. Remember, my blogs are designed to make you think.

So, think about this: Fraud is not predictable as to when it will occur but is fairly straight forward as to how it will occur.

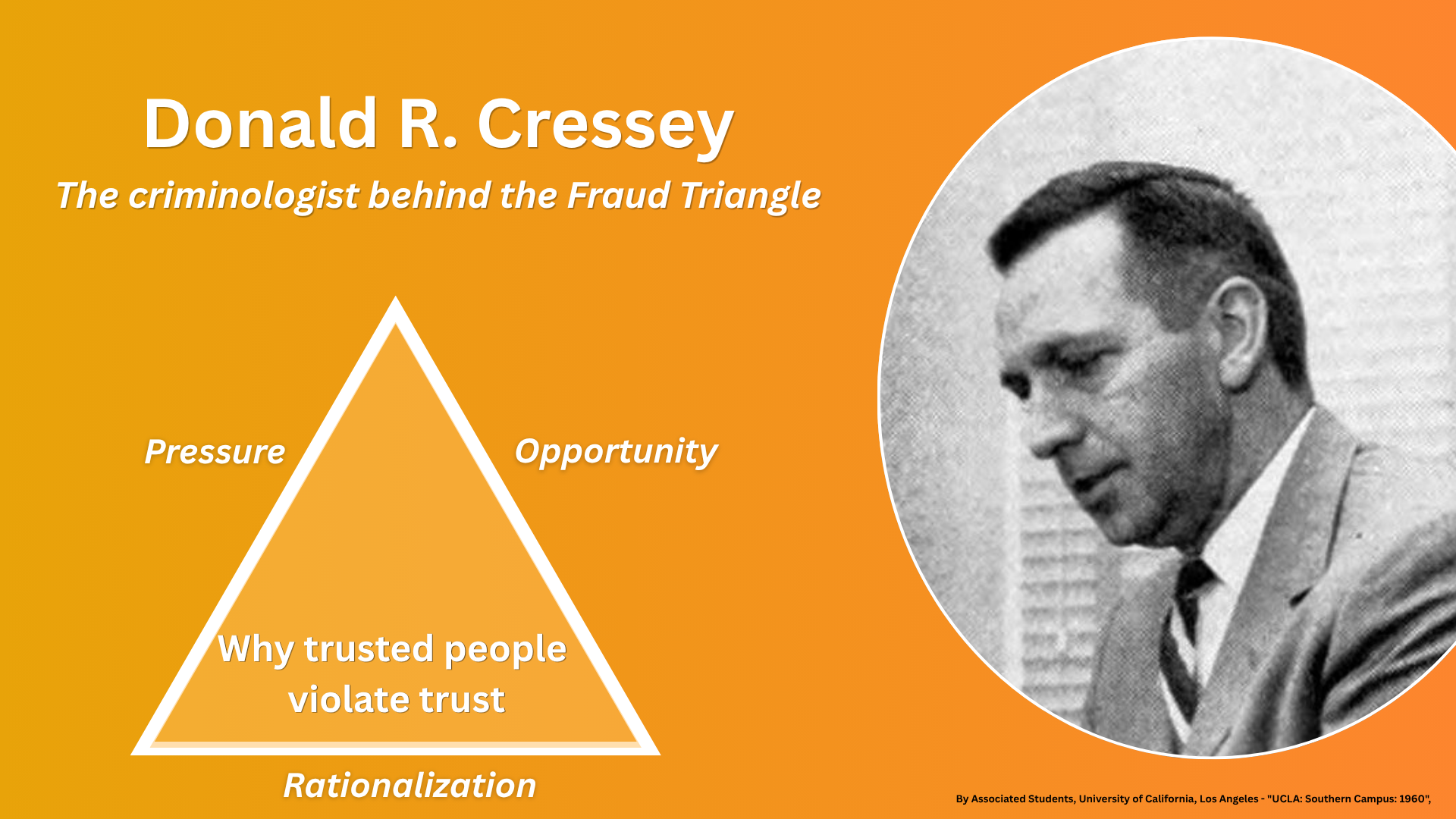

Many years ago, the IT auditor was created. In fact, I was an IT auditor in 1979. For the last 40 years, however, I have been a fraud auditor. Unfortunately, unlike IT, the profession does not recognize the title of fraud auditor.

In my opinion, it is time for the title of Fraud Auditor to be created and recognized by the profession. Auditors are not born with fraud risk or fraud audit knowledge or fraud skills. I suspect that college courses are not designed to provide this knowledge. If the profession is serious about a “more proactive approach to fraud detection” it is time to recognize that this will require auditors to develop and gain a new set of skills. I recommend that every audit department invests in human fraud risk intelligence.

Current audit standards call for us to use a mitigation standard when it comes to audits This means that unless you want to be an outlaw, your assessment will end with mitigate. However, the question I want you to ask yourself is, right now do we have enough information to properly assess the mitigate question?

This month I will present at a conference a new approach to fraud risk assessment. It is the cumulation of my 40 years of experience in building the fraud audit model.

In this series of blogs, we are looking at the practice of using a fraud audit to detect shell company schemes occurring in an accounts payable file. Because the practice of effective fraud auditing is grounded in knowledge, we will start with a knowledge section and then delve into a demonstration of the fraud audit process.

In this series of blogs, we are looking at the practice of using a fraud audit to detect shell company schemes occurring in an accounts payable file. Because the practice of effective fraud auditing is grounded in knowledge, we will start with a knowledge section and then delve into a demonstration of the fraud audit process.

In this series of blogs, we are looking at the practice of using a fraud audit to detect shell company schemes occurring in an accounts payable file. Because the practice of effective fraud auditing is grounded in knowledge, we will start with a knowledge section and then demonstrate the fraud audit process.